Financial Steps a Newlywed Couple Needs to Take for Their Future

2019-09-13

How to plan for your financial future

You just got married. Now what? Besides jetting off for your honeymoon, there are actually a handful of financial matters that a newlywed couple needs to take note of in order to start on a financially secure path.

From financial goals to joint accounts, property ownership to legal wills, we talk to Financial Services Manager Joseph Tan to better understand these first few financial steps a couple needs to take together.

Set your goals first

Before you take any action, you need to first decide what you wish to accomplish as a married couple. While financial goals can be along the lines of aiming to save a certain amount of asset – say, $4,000,000 by x number of years – oftentimes, couples end up purchasing assets instead as a form of savings.

This can mean purchasing a new house even before hitting their target of $4,000,000, and this then leads to loans and instalments to take care of, which will require couples to carefully consider if they can afford to consistently pay up those loans and instalments. To do that, these are some questions that you will have to consider:

- How much are you earning?

- How much debt do you currently owe?

- How much do you have in the bank?

- Are you planning to change or leave your job soon?

Therefore, it is of utmost importance to think carefully about what you want in the future, discuss them with your spouse, and then commit to them. Otherwise, your original financial plans will be derailed and whatever steps you’ve taken up till then may be insufficient to prepare you for your newly minted goals. This brings us to the two aspects of planning for a future together that couples must consider.

The psychological aspect of financial planning

Even before a couple gets married, they need to understand and acknowledge that once they do, they are both equally responsible for contributing to the marriage – be it emotionally or financially.

This means being completely transparent with one another in terms of salary, expenditure, and financial goals, and it helps to not only allow you to plan appropriately for the future that you have envisioned together, but also to build trust as husband and wife.

Once you have all these out in the open, the next step is to define your individual roles in the relationship and then commit to them – this is to prevent indignant complaints and disagreements in the future!

Generally, there are three ways a husband and wife can work together at supporting their marriage:

- One person will handle all the expenditure, while the other will be in charge of earning money

- Both parties contribute to expenditure equally

- Both parties contribute to expenditure in proportion to what they earn.

On that note, make sure that the goals and roles set are reasonable for both parties. For example, if you both agree to aim for a landed property within the next 10 years and yet the wife is a stay-at-home-mum while the husband is the sole breadwinner, it is important to note that this may put a lot of pressure on the latter to earn enough to be able to achieve that goal while putting food on the table.

The legal aspect of financial planning

The legal aspect of financial planning refers to secure ways to provide for your loved ones in the event that you unfortunately die, or become unable to provide for them financially.

Whether you want your money to go to your parents, your spouse, or both of them will depend heavily on these 4 arrangements:

1. Make a will

In Singapore, wills are governed by the Wills Act, which states that a testator may devise, bequeath, or dispose of his real or personal estate via a will. This will dictate how all of your assets – apart from jointly-owned bank accounts and houses – will be split to your beneficiaries (who you’re giving the assets to) and their guardians if they are still too young.

There must also be a revocation clause to revoke any and all previous wills, and each time you wish to amend your will, you will have to rewrite the entire document for about $300 - $500.

2. Property ownership

Most newlyweds would probably be looking for a home of their own. When you purchase a property, such as a BTO flat, you will be asked to choose if you wish to hold Joint Tenancy or Tenancy-in-Common, and this decision can only be made at the point of purchase or transfer of ownership.

In Joint Tenancy, the joint owners basically co-own the entire property. There are no separate shares, so in the event of your demise, your spouse will take sole ownership of the whole property, regardless of whether or not you’ve left behind a will that states otherwise.

On the other hand, tenants-in-common own the same property in separate shares – for example, 60:40. This means that if you pass away, your spouse will only be legally entitled to her share of the property, and your share will be split accordingly to however you’ve dictated in your will.

3. Insurance policy nomination & CPF nomination

Another way to ensure that your loved ones are financially taken care of as per your wishes in your absence is through insurance policy nomination and CPF nomination. These are arrangements to determine who gets your insurance proceeds and CPF monies in the event of death (or permanent disability for insurance).

For insurance policy nomination, nominees can be your family members, children, spouse, or any other persons, and there are 2 types available: a trust nomination, also known as an irrevocable nomination, and a revocable nomination. Depending on which type of nomination it is, you may or may not use your will to override that nomination to change your initial beneficiary.

As for CPF nominations, you may nominate any person below 18 years of age as your nominee and determine the share he/she will get of your CPF monies in your Ordinary, Special, Medisave and Retirement Accounts, unused CPF Life premiums, and discounted SingTel shares if any.

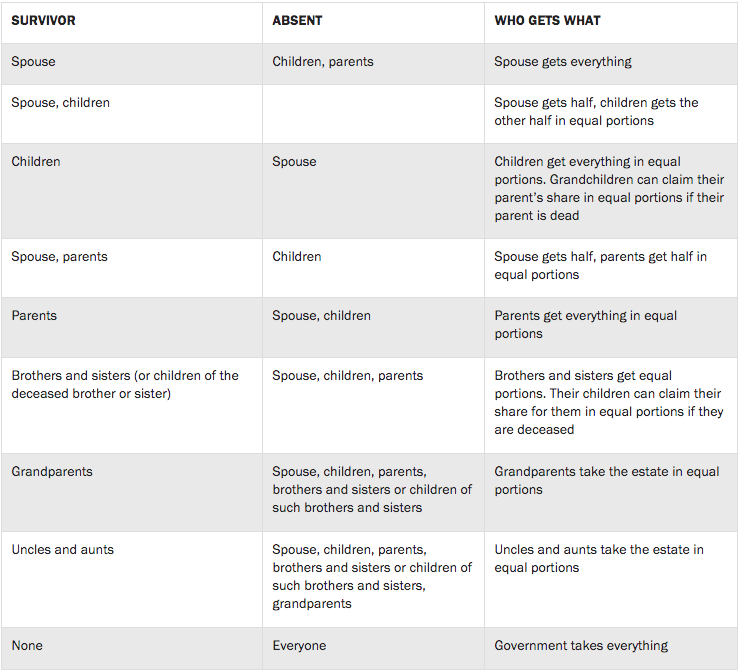

Without such nominations, your insurance payout and CPF monies (not including discounted Singtel shares) will follow the intestacy law under the Intestate Succession Act (ISA) for non-Muslims or the Muslim law for Muslims and be distributed by an administrator in the following order after all owed taxes and debts are paid:

Source: Singapore Legal Advice

4. Joint bank account

Finally, a couple should always open joint bank accounts after they get married. Besides helping to build trust knowing that both parties are contributing to support the marriage and your shared goals, it’s a good way to provide emergency funds for your surviving half to cover the funeral expenditure and other daily needs until he/she manages to become financially stable on his/her own.

If you’re unsure how much needs to go into this joint account, the general rule of thumb is to have at least 3 to 6 months worth of rainy-day-fund, which is the average amount of time needed to find new employment.

As for how much each party should add to the joint account each month, it is entirely up to the couple themselves to decide, although most usually contribute based on how much they are earning – i.e. 10% of their monthly salary.

Should something unfortunate ever happen to you, all your surviving spouse needs to do to gain access to the joint account is to provide the bank with a copy of your death certificate and bring proof of identity (passport or NRIC).

Note: This is provided that the joint account is not pledged to a liability of the bank, such as an overdraft.

For more advice on planning for a financially secure future together as a couple, reach out to Financial Services Manager, Joseph, at 9853 0208.

Request a quote from over 450 wedding vendors

Get A Free Quote Now

The Art of "I DO" | Mondrian Singapore Duxton

GET THE APP

WE ACCEPT

Copyright © 2026 Citrus Media Pte. Ltd.

Reg No.: 200206092Z. All Rights Reserved